Posted: Tuesday, April 2, 2024

Word Count: 1850

Reading Time: 9 minutes

Organizations such as Fundrise, Arrived, and Lofty.ai are examples of companies that operate within this realm. PropTech fintech blends finance, technology, and real estate investment, aiming to make it more accessible and manageable for a broader audience. They offer an easy way for the average person to invest in the real estate market and broadly remove the risks usually associated with real estate investments. At a high level, these companies perform the following:

- Purchase or invest in real estate properties.

- Offer investment opportunities for as little as $10 in some cases.

- Rent out these properties in most cases.

- Investors receive a portion of the rent and property appreciation as a return.

- Returns are either distributed as a dividend or via ACH transfer.

They all share the common goal of simplifying, demystifying, and democratizing access to real estate investments. By leveraging technology, they reduce barriers such as high entry costs and complex management logistics, making real estate investment more akin to ordering your food online rather than cooking from scratch.

Here’s a comparison table for the discussed offerings:

| Platform | Purpose | Minimum Entry Investment | Expected Returns |

|---|---|---|---|

| Fundrise | Enables individuals to invest in diversified portfolios of real estate assets through an online platform. | Typically $10 – $1,000, depending on the account tier. | Historically, returns have ranged from approximately 8% to 12% annually, though this can vary based on market conditions and portfolio selection. |

| Arrived | Offers shares in single-family rental properties, allowing investors to earn passive income without dealing with the responsibilities of direct property ownership. | As low as $100 for a share in a property. | Returns are generated through rental income and potential property appreciation, varying by property and market conditions. |

| Lofty.ai | Utilizes blockchain technology to allow for fractional real estate investment, with each token representing a share of property ownership. | As low as $50 for a token in a property. | Returns are based on rental income and property appreciation, similar to Arrived, but with additional liquidity options through tokenization. Returns vary widely based on property performance and market trends. |

However, there’s a growing concern that, despite their stated goal to empower the average American, they are exacerbating the housing affordability crisis.

The Dream is Fading

While many nowadays say the dream is gone, housing affordability is at an all-time low. In the last few years, home prices have appreciated at an astonishing rate, fueled by a robust job market and once-in-a-lifetime, bargain-basement interest rates. The competition in many markets was so fierce that homes were often purchased sight unseen, with buyers foregoing repairs.

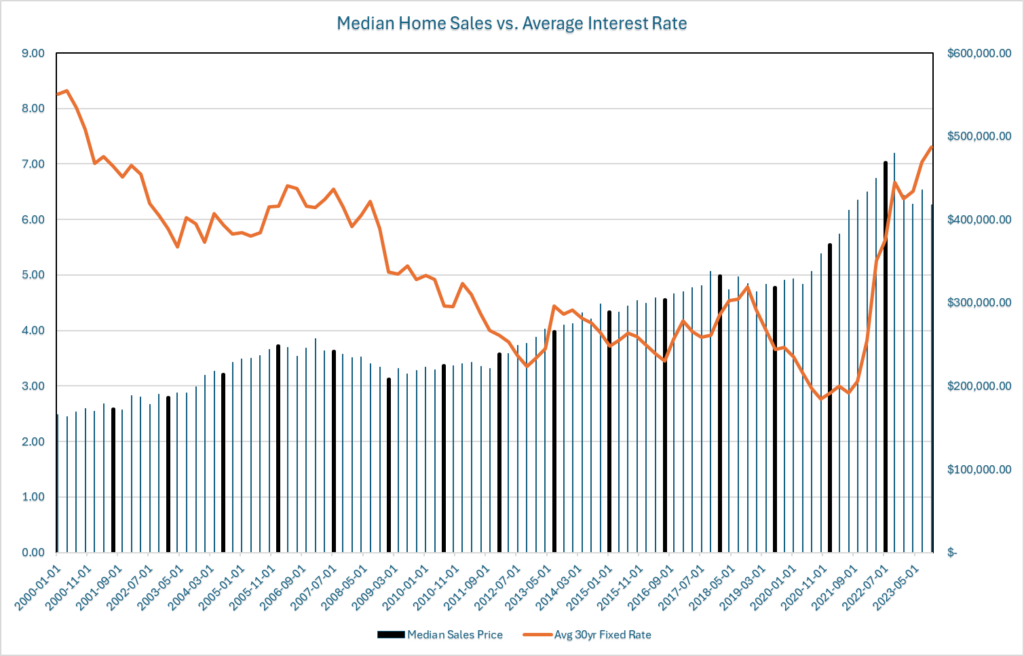

As the table below shows, historically, real estate appreciates over time. Even the Great Recession didn’t significantly impact the overall average home sale price. During the height of the pandemic, the Federal Reserve began aggressively cutting rates to stimulate economic activity, and Americans responded en masse. Many seized the opportunity to purchase or refinance their homes. Lower interest rates also made it possible for people to afford homes that may have previously been financially out of reach, contributing to the rapid appreciation in real estate prices.

Here Comes the Feds

The Federal Reserve stepped in and raised interest rates in an effort to stabilize inflation. They embarked on a campaign of aggressively and rapidly increasing the federal funds rate. Historically, raising rates, when done judiciously, has been effective in controlling inflation. However, it can also inadvertently trigger a recession and/or stagflation. The objective was to temper inflation without inciting a recession—a challenging balancing act, despite what many critics have claimed.

The economy seems to be reacting to the rate increases, with inflation moderating somewhat; however, home values have shown surprising resilience, even as the volume of overall home sales has declined. There are several reasons for this:

Housing Inventory Remains Low

- Constrained Construction: Rising rates have a dampening effect on construction activity. Developers often rely on borrowing for financing their projects, and higher interest rates mean higher borrowing costs, leading to a slowdown in new developments.

- Homeowner Reluctance: With the rates previously being below 3%, homeowners are disincentivized to sell because it would mean giving up a low mortgage rate. Unless necessary, staying put is financially more appealing.

- Downsizing Deterrent: Downsizing typically implies moving to a less expensive, smaller property, but in a market where prices are high and rates have risen, this move might not result in lower monthly costs. Therefore, it can be financially counterintuitive for homeowners to downsize in the current climate.

Unemployment Remains at Historical Lows

- Employment Over Income Growth: Even though wage growth has been sluggish and hasn’t kept up with the cost of living or inflation in many areas, employment rates are high. This indicates that people are choosing to stay in their jobs despite the stagnation in wages, possibly due to the security that employment offers in uncertain economic times.

Rate Changes Don’t Affect Locked-in Home Mortgages

- Stability of Fixed-Rate Mortgages: Most homeowners with fixed-rate mortgages, including those who refinanced during the period of historically low rates, are insulated from the direct impact of rate hikes. Their monthly payments remain constant, so there is no immediate financial pressure to sell their homes.

- Scarcity of Adjustable-Rate Mortgages (ARMs): There’s a lower prevalence of ARMs in the market currently, which means fewer homeowners are subject to the volatility of fluctuating interest rates, thus reducing the urgency to sell due to rate increases.

The table below compares the interest rate to the average sale price over the past 20 years. Even with interest rates jumping from 3% to over 7% over the last 2.5 years, median home sales over recently dipped.

Salaries haven’t kept up with inflation

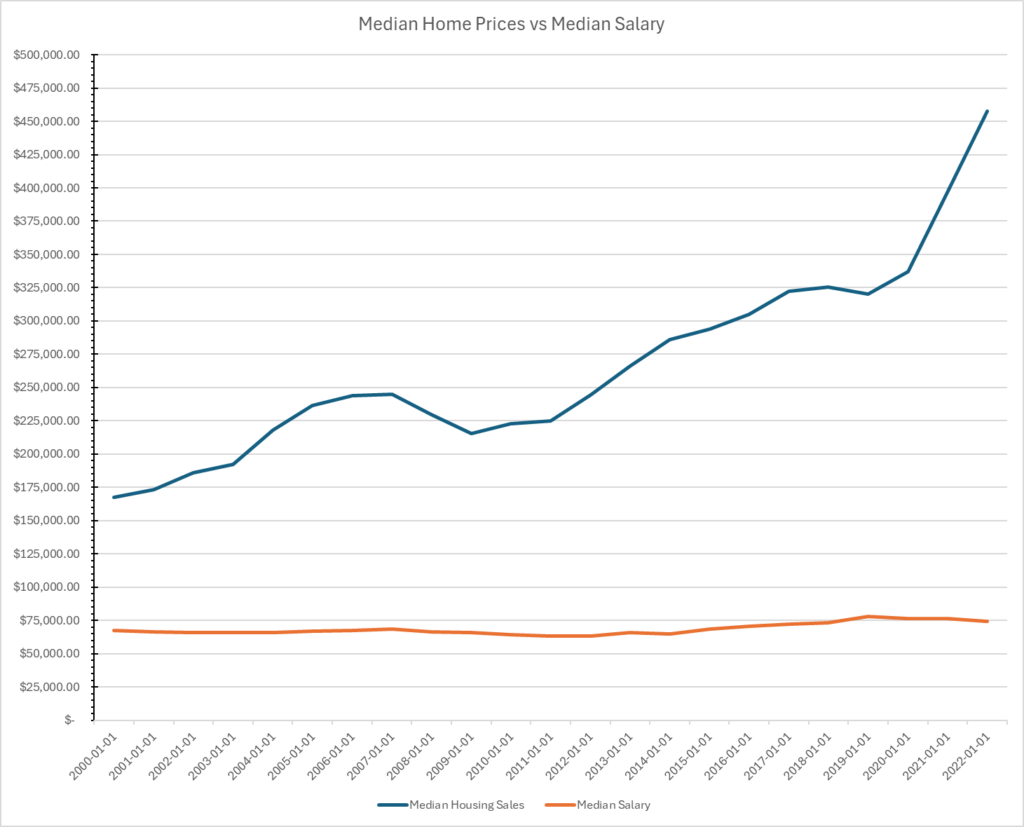

Although the unemployment rate remains relatively low, wages have not kept up with inflation. The chart below compares home appreciation to the median Salary in the US. Compared to the real estate market, wages appear to be relatively flat.

The chart tells a simple story, the cost of homeownership takes a much larger chunk of today’s paycheck.

Even before PropTech enters the conversation, the current economic landscape already handicaps many prospective buyers.

The Growing Concerns as PropTech Matures

I should take this opportunity to mention that I’m an active investor in Lofty, Fundrise, and Arrived. I would say that I pretty much dive into any novel investment strategy. In addition to the aforementioned, I have money sprinkled across other platforms like Mainvest and Prosper. Now that being said, many of the concerns about this growing market are arguably inconclusive at this stage but remain quite valid.

The fact remains that these companies are securing homes across the 48 contiguous states that otherwise would have been available to Joe and Jane American. I was unable to locate any data that provided detail into how many properties were purchased by PropTech companies, but the Arrived investment page lists 362 properties on their website, which is a relatively small amount when compared to the total number of properties that are listed for sale in the US (at the time of writing, approximately 1,396,264 homes according to Redfin). However, that may skew reality, since PropTech companies concentrate on specific regions and could greatly affect the local market while not impacting US real estate trends nationally, and with such low inventory levels, losing one property to the man or woman can be enough to tip Americans against these companies.

Furthermore, the liquidity behind these organizations can easily outcompete a prospective buyer trying to purchase a home with some pre-approved letter. Cash offers fast track the process with the seller and remove control gates such as home inspections.

Finally, the properties they’re purchasing are then converted into long-term and/or vacation rentals, effectively removing them from the market for the foreseeable future. This also supports the narrative that America is becoming a nation of renters.

It’s easy to see how PropTech companies are continually being seen as a hindrance to homeownership.

It’s Not All Bad

However, there’s another perspective to consider. These companies are not entirely a source of doom and gloom. Beyond the investment opportunities they provide, there are inadvertent positive contributions they may be making to the real estate market.

Positive Effect on Existing Property Values

Purchases by these companies often occur at or near the market value of the property, supporting neighborhood property values. These are not foreclosures or short sales that could potentially depress nearby home prices.

Improving Neighborhood Appeal

These companies typically maintain and update their properties, which can positively influence the overall appeal of the neighborhood.

Rentals are Long-Term (Mostly)

The majority of properties acquired by PropTech companies are designated for long-term leases (12 months or more). For instance, Arrived usually targets renters looking for leases of 15 months or longer. Such extended leases provide stable returns for investors and foster community integration among renters. Admittedly, while Arrived does offer both long-term and vacation rentals, the substantial portion of their portfolio is dedicated to long-term tenancies.

My Take On It

Although I agree that their business model does remove houses from the market, they also present an opportunity to create passive income and offer an entry level into real estate investment.

It Offers Another Investment Opportunity

REITs have always existed in one form or another. However, many of them require a substantial investment to get started. PropTech companies’ low entry barriers allow anyone to start investing, empowering younger generations to invest early and leverage the power of compounding interest to create a passive income. The table below provides a monthly passive income estimate based on a consistent weekly investment.

| Year | $10/week | $25/week | $50/week | $75/week | $100/week |

|---|---|---|---|---|---|

| 5 | $9.98 | $24.95 | $49.90 | $74.85 | $99.80 |

| 10 | $23.12 | $57.79 | $115.59 | $173.38 | $231.17 |

| 15 | $40.41 | $101.03 | $202.05 | $303.08 | $404.10 |

| 20 | $63.17 | $157.93 | $315.87 | $473.80 | $631.73 |

| 25 | $93.14 | $232.84 | $465.69 | $698.53 | $931.38 |

| 30 | $132.58 | $331.45 | $662.90 | $994.35 | $1,325.81 |

| 35 | $184.50 | $461.25 | $922.51 | $1,383.76 | $1,845.01 |

If you choose to pick up your takeout orders instead of using food delivery services, you can redirect that money toward creating passive income. As the table illustrates, even investing as little as $10 a week can accumulate over time. The passive income listed displayed in the table assumes a 5% appreciation rate and a 4% drawdown.

Would Eliminating PropTech Really Solve Anything?

Perhaps it’s the cynic in me, but I don’t believe that prohibiting PropTech companies from purchasing properties would ultimately resolve the broader issue. There are other REITs and real estate entities converting single-family homes into rentals and not sharing their profits in the same manner. A blanket ban on such activity wouldn’t prevent other affluent individuals from acquiring these homes. Put simply, where there is a profitable opportunity, someone will capitalize on it.

Retirement Options are Limited

Moreover, remember that the Social Security “lockbox,” established after the Great Depression, is no longer solvent in its current form. All the solutions proposed so far would lead to reduced benefits or an extended waiting period for eligibility. Many have accepted the likelihood of working well past the traditional retirement age of 65.

It seems inevitable that local, state, and federal governments will intensify their scrutiny of these sectors. However, before any legislation is enacted, we must be careful that our efforts to alleviate one problem do not unintentionally aggravate another.

Leave a Reply