Posted: Saturday, January 13, 2024

Word Count: 3657

Reading Time: 16 minutes

Crypto remains a mysterious and divisive topic. The value of most, if not all, coins is highly speculative, and governments are torn between supporting, controlling or regulating cryptocurrency to extinction. Financial experts, including Warren Buffett and Charlie Munger, have been outspoken critics of crypto, predicting its demise. Commercials even poke fun at meme cryptocurrencies like Dogecoin and Shiba Inu. The recent crypto winter has only emboldened these experts, who are advising people to abandon cryptocurrency. Admittedly, crypto has taken a significant hit in the past year and a half, losing over 80% of its value during that time. Despite all this, the crypto industry remains and arguably have clawed back some of the losses experienced in 2022. Why hasn’t crypto failed. It boils down to a single word…. Hope.

In the beginning, there were the Baby Boomers

Not the say that baby boomers had the easiest life. To be fair, Vietnam was no walk in the park, and they certainly had their fair share of recessions. However, they also grew up during one of the most prosperous times in the United States. World War II, catapulted the United States as the undisputed world leader. What followed was a time known Known as the golden age. It was a period of economic prosperity with the achievement of high and sustained levels of economic and productivity growth. Homeownership was arguably easier to obtain at that time. Manufacturing was on the rise, allowing those without advanced degrees to live a comfortable life.

The College Path is broken and tattered

By the late 70s, things began to shift. Domestic manufacturing began to compete with offshore industries. In order to drive down prices, manufacturing began shifting near and off-shore leading to factories being shutdown and people losing their jobs

Baby Boomers, now parents, who lived to see their communities collapsed when the local plant was shutdown or scaled back, began to see that living in America without a degree, would be difficult. They encouraged children to attend college to obtain degrees, and many GenXers and millennials listened. They listened to how college debt is a good thing. Something that would pay you back a thousand-fold. They were told to seek prestigious universities and expensive degrees.

In some instances, we were told that the type of degree didn’t matter, as long as you obtained one. As more of us poured our souls into a college degree, alternative colleges arose to offer accelerated degrees with implied guarantees of employment.

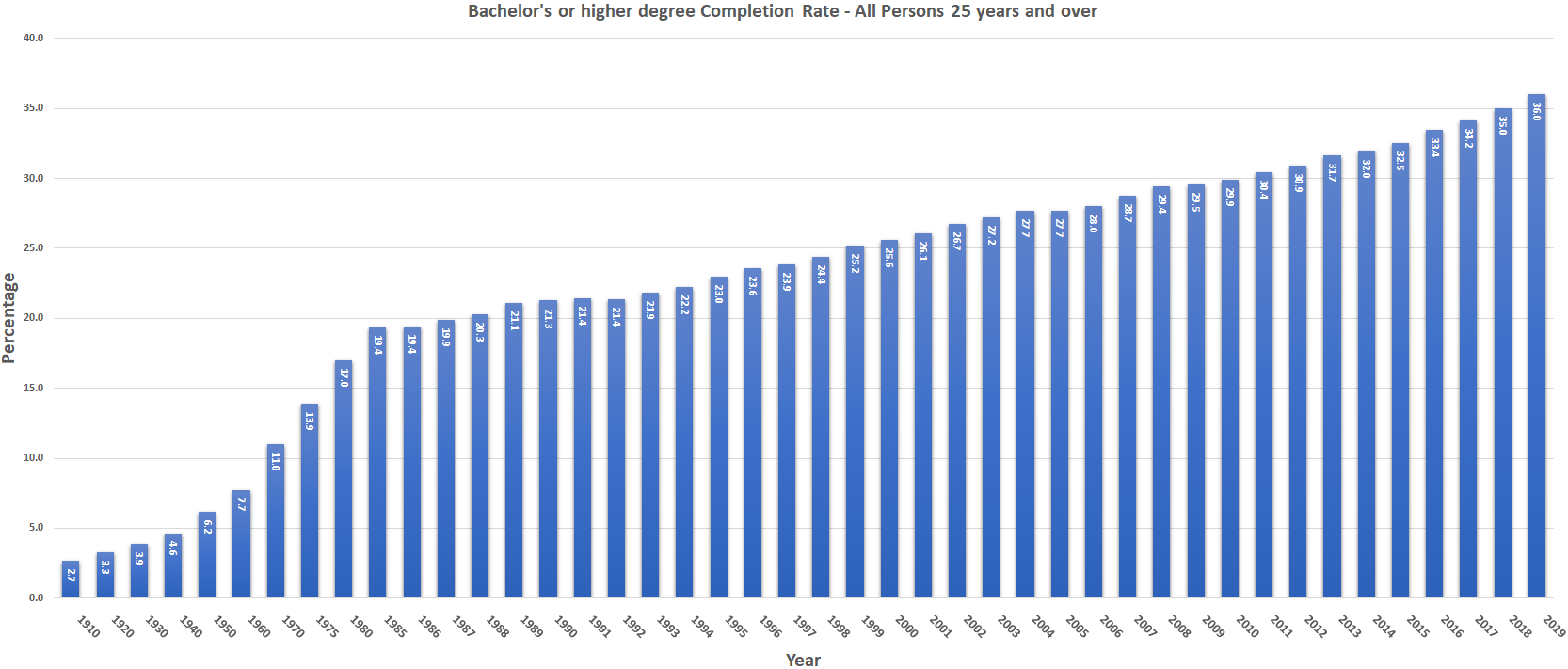

Consider the following charts:

In the 1990s, the high school graduation rates we in the low to mid-80 percentile and college graduation rates hovered around 25 percentile. This shows how obtaining a high school diploma in the 80s and 90s would have not completely excluded you from obtaining a career that could support yourself and potentially a family.

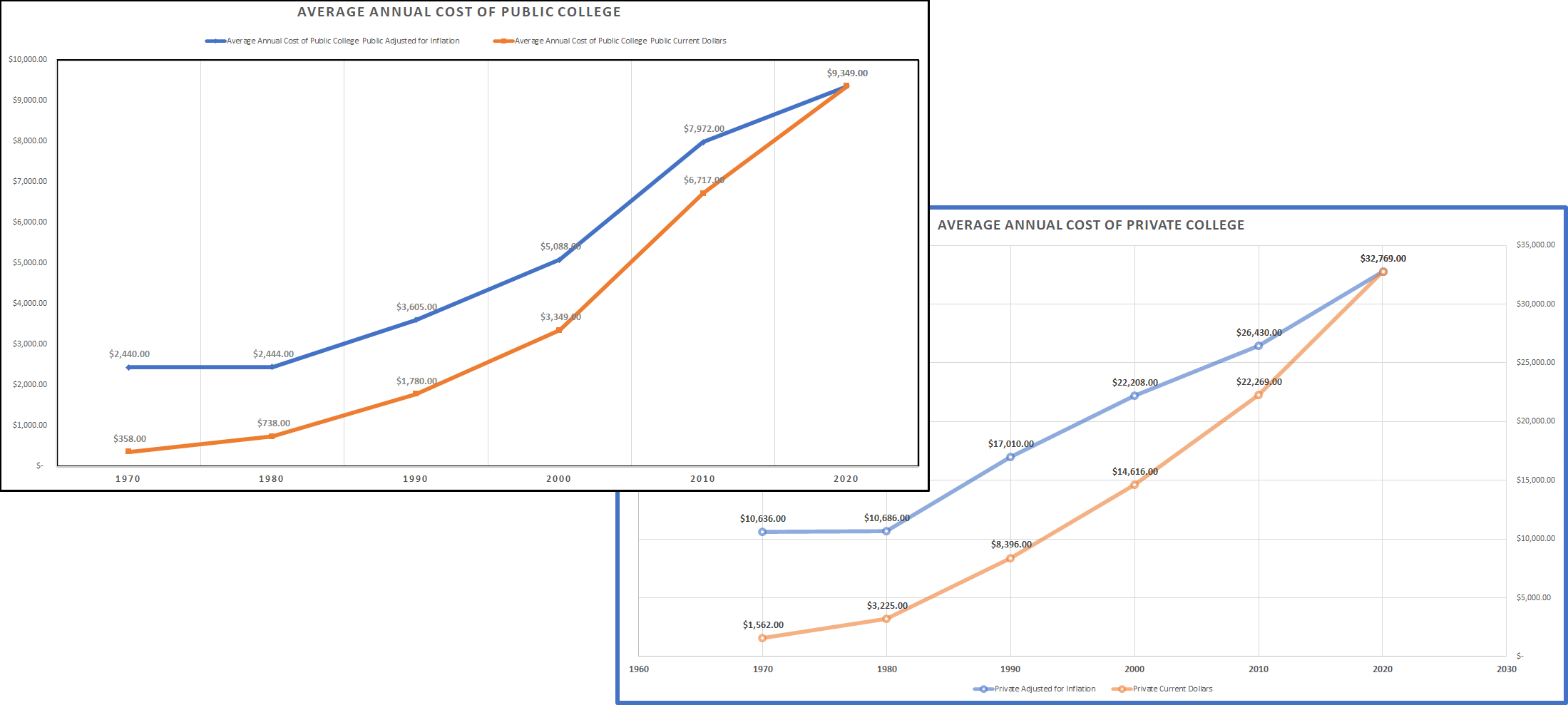

College was never cheap

However, as college education continued to be embraced as a guaranteed path to the American dream, the cost of tuition rose rapidly. Even adjusted for inflation, the annual cost to attend a public and private college cost almost 4 times and 3.1 times (put it another way 400% and 300% increase)respectively, as much as it did in the 1970s.

College Degree Devaluation

By the turn of the century, it was assumed that most children would attend a 2yr or 4yr college. The number of adults with a 4 year degree increased substantially. Thus began the devaluation of the college degree. No longer could you just obtain a degree to get ahead. Parents began to dissuade children from following their passions in psychology, social work, theology and focus on high paying degrees in Engineering, Information Technology, Economics and Finance.

Everyone was on a mission to obtain a degree, by any way possible. The streets were lined with billboards and the airwaves flooded with commercials (usually late at night) that advertised schools such as ITT Technical Institute as an alternative to the traditional college experience. They would tout their ability to change lives boasting over 90% of their graduates found employment after graduating. They would guarantee a degree in an accelerated time line: months instead of years. They promised flexibility and partnerships with big companies. The reality was no where near that guarantee, and in some instances finding employment after the degree didn’t necessarily mean you found employment in your chosen field.

The job market became flooded with candidates with degrees from various colleges and institutions. The edge a degree provided began to erode for many. Today, it not only matters that you have a degree and its specialty, but from what institution you obtained it from.

The Debt Piles on

Unfortunately, all that glitter isn’t gold and all that debt isn’t that great. Although degrees can get your career off the ground, they will not necessarily command a large salary early on. The average student loan debt incurred for private and public institutions is $54,921and 37,338 respectively per borrower. Paying off this debt while attempting to live your life can be difficult. According to the US News, the average monthly student loan payment is roughly $300 on a 10 year payment plan. The US bureau of Labor Statistics states the average hourly range for a degreed individual in the United States hovers at $1620 per week or $84,240 annually. However college isn’t the only thing that has increased in price, everything has. So assuming a $84,240K annual salary and a $300 payment. let’s see how much money is left over after expenses.

| Categories | Annuals | Catalyst |

|---|---|---|

| Gross Income | $84,240 | Before benefits, taxes and other deductions this salary doesn’t look that bad. |

| Benefits | $5527.20 | Assuming $3000 annual cost for single medical + 3% to the 401K |

| Taxes | $17,842.56 | For an individual earning $84,240 per year, the applicable federal income tax bracket for 2023 is 22%. This rate applies to single filers with an income that falls within the range of $41,775 to $89,075. |

| College Payment | $3,600.00 | 12 payments of $300 / mo. |

| Car Payment | $8700.00 | Average cost from nerdwallet is $725 for new vehicles Link |

| Car Insurance | $2148.00 | NerdWallet estimated $179.00 per month. Link |

| Car Maintenance | $1200.00 | Average car maintenance for a relatively reliable car would cost $100 per month. Link |

| Gas (Petrol) | $3556.80 | The current national average is $3.80. Assuming a 12 gallon tank, and filling the tank once a week cost $68.40 filling up 1.5 times per week. Link |

| Rent | $23,736.00 | National Median for rents in the US is currently $1978.00. Link |

| Utilities | $5151.96 | The national average cost of utilities in the United States, as of 2023, is approximately $429.33 per month. Link |

| Streaming Services | $186.00 | Minimally, I would expect at least one paid streaming service. Netflix standard currently hovers around $15.50 / mo. There are some decent free services out there like Tubi that should curb this cost a bit. |

| Groceries | $3432.00 | This assumes a weekly spend of $66 per week. Even at today’s prices a single person should be able to grab more than just ramen noodle. |

| Clothes | $3400 | According the NerdWallet the average American spends $3400 – $7000 per year on clothing |

| Remaining | $5759.48 | Seems like a lot, but… |

So our exercise leaves us with almost $6000 surplus after all the required stuff is taking care of, and that sounds like a lot, but what this exercise cannot account for is the other stuff. For instance, the utilities include a single mobile phone plan, but does not actually account for the procurement of that phone. A decent phone today starts at roughly $450 brand new although the pre-owned market is an option as well. Furthermore, the rent is accounted for, but not the procurement of everything that would actually go into an apartment. Furniture, Beds, TV sets and more all add up and chip away at what’s left. Then there’s Christmas, Valentines, Halloween and Birthdays that can potentially hit your savings. Keep in mind, that you’re somehow supposed to use your PTO and do something enjoyable once a year. Finally, the unplanned things family emergencies, accidents, all the unforeseen things life throws at you. All that to say this: the cake is a lie and that remaining balance is probably being allocated for some other need or desire.

Now I’m not necessarily saying that a college degree isn’t worth it, and there are many examples where people achieved their degrees and succeeded in their career field. However, there are many more whose dream fell short and their college journey left them with either debt or a useless degree. A special type of debt that cannot be erased by bankruptcy which means it can weigh on you the rest of your life theoretically. There are many individuals that haven’t seen a college classroom for 20 plus years still being reminded of their shortcoming every month when their student loan comes due. Finally, there are those that attended an educational institute that has since shutdown effectively making their degrees no more valuable than the paper it was printed on. However, the debt they incurred would disagree.

Recessionpaloosa

Many of us grew up with parents that saw the financial benefits of homeownership. By 2000, pensions for the most part have been relegated to the very few. 401K, As, 403B and other retirement accounts largely replaced pensions. The government allows you to invest pre-tax monies into these accounts, don’t worry they’ll take their cut on the other side.

Additionally, the information age introduced online trading, allowing easy access to buy and sell stocks. Articles were written about 17 year olds that turned $100 into $1,000,000. However, that not something that most people experienced.

Let’s reset, I’m not saying in anyway that 401K and other retirement funds are a bad idea, in fact, I’m an advocate. However, they do not compare to the financial security of a pension and do not account to the needs of the individual at that time. I would assume most people would love to invest 15% of their pre-tax pay check into a retirement fund, the problem is, many folks don’t have 1% to spare.

And as the millennials and your genXers were entering the workforce several major events have presented major roadblocks to financial security. Let’s discuss a few in the next section.

The Recessions: A Brief Overview the struggle of the Millennials and the young genXers

Dotcom Bubble (March 2001 – November 2001)

Catalyst: The dotcom bubble burst was primarily due to the overvaluation of internet-based companies. Investors poured money into internet startups with the expectation of rapid growth. However, many of these companies lacked sustainable business models and tangible earnings. The burst led to significant stock market declines and the failure of numerous dotcom companies.

Impact: This period saw a loss of investor confidence, particularly in technology stocks, and led to substantial financial losses, job cuts, and a reevaluation of investment strategies in technology-based companies.

Mortgage Crisis aka the Great Recession (2007 – 2009)

Catalyst: The financial crisis was triggered by the collapse of the housing bubble, leading to massive losses in subprime mortgage loans. The fall of financial giants like Lehman Brothers created a domino effect, severely impacting the global economy. This crisis led to the Great Recession, the most severe economic downturn since the Great Depression.

Impact: The crisis resulted in significant job losses, home foreclosures, and diminished savings for many Americans. It eroded trust in financial institutions and highlighted systemic issues in the banking and real estate sectors. The Federal government stepped in to prop up many large enterprises or facilitated mergers to prevent further fallout. The table below lists a few large enterprises that were dramatically affected by the Mortgage Crisis.

| Company | Detail |

|---|---|

| Lehman Brothers | Perhaps the most famous casualty, Lehman Brothers filed for bankruptcy in September 2008, which was the largest bankruptcy filing in U.S. history at the time. |

| Bear Stearns | This investment bank was another major victim. It was sold to JPMorgan Chase in March 2008 in a fire sale triggered by a liquidity crisis. |

| AIG (American International Group) | AIG faced a liquidity crisis due to its involvement in the mortgage market, leading to a massive bailout by the U.S. government. |

| Merrill Lynch | Struggling with losses from the subprime mortgage crisis, Merrill Lynch was acquired by Bank of America in September 2008. |

| Fannie Mae and Freddie Mac | These government-sponsored enterprises played a significant role in the expansion of the subprime mortgage market. Both were placed into conservatorship by the U.S. government in 2008. |

| Countrywide Financial | Once the biggest mortgage lender in the U.S., Countrywide was acquired by Bank of America in 2008 amidst serious financial struggles. |

| Washington Mutual | Known as WaMu, this was the largest savings and loan association in the U.S. It was seized by the Federal Deposit Insurance Corporation (FDIC) and sold to JPMorgan Chase in 2008. |

| Wachovia | This was one of the largest bank holding companies in the U.S. before being acquired by Wells Fargo in 2008 after facing a severe liquidity crisis. |

| Citigroup | Citigroup suffered significant losses during the crisis and received a substantial government bailout to prevent its collapse. |

| General Motors and Chrysler | While not financial firms, these automotive giants were significantly affected due to the economic downturn and credit crunch caused by the mortgage crisis. Both companies underwent government-backed bankruptcies and restructuring. |

The general approximate combined valuation of these organization just before the great recession was roughly $878 billion. As you can surmise, 1 trillion dollars being forcefully yanked from the economy would have been even more devastating than what we experienced.

The Federal Reserve and 2023 Recession

Catalyst: The looming recession of 2023 is attributed to the Federal Reserve’s efforts to control inflation. The Fed raised borrowing costs to slow down economic growth and curb inflation, which had been rising at a concerning rate. However, this aggressive monetary tightening raised fears of a severe economic downturn.

Impact: The full impact of this recession is yet to be fully understood, but it has already started affecting consumer confidence and market stability. There is growing apprehension about job security, investment returns, and the overall health of the economy.

Each of these economic downturns profoundly affected many young Americans, particularly as they were just beginning their careers. Beyond the defined timelines of these crises, their effects rippled through the economy long after their official conclusion. The mortgage crisis, for instance, trapped numerous individuals in a state of credit paralysis, hindering their ability to reapply for mortgages. The proximity of these events meant that many barely had time to recover from one crisis before being struck by another, exacerbating the financial strain. Additionally, in an effort to navigate these turbulent times, a significant number of people were compelled to withdraw funds from their retirement savings, incurring substantial tax penalties and jeopardizing their financial security in later years.

The Church of Crypto

Crypto moves far beyond the boundaries of traditional investments and currencies, these digital assets have cultivated a following that can only be likened to a church congregation in its intensity and devotion. This is a world where the lines between investment strategy and personal identity blur, creating a landscape teeming with an almost evangelical belief in the power of their chosen digital currencies.

Platforms like Telegram and X, formerly Twitter, have become the digital temples of this movement, where folks gather not just to exchange tips or analyze trends, but to champion their chosen cryptos with a mix of savvy marketing and unshakable faith. On these platforms, cryptocurrencies are not merely assets to be traded but banners to be waved in a financial revolution. Posts and threads aren’t just discussions; they’re sermons preaching the potential of a decentralized financial future. These are the folks that continue to encourage folks to Hold on for deal Life (HODL) regardless of how far the value the of their coin drops.

In this realm, cryptocurrencies are bolstered by an eclectic mix of libertarians, technophiles, investors, and dreamers, all united by a shared vision of disrupting traditional financial systems. This section delves into the unique cultural and social dynamics that have turned cryptocurrencies from a niche digital experiment into a global phenomenon with a cult-like following. We’ll explore how this fervent community, powered by social media and driven by a blend of ideology and investment, has become a defining feature of the crypto world, setting it apart from the more staid and regulated realm of traditional finance.

The Dogecoin Phenomenon

Background: Dogecoin, originally created as a joke based on a popular internet meme, quickly evolved into a legitimate digital currency. Despite its humorous beginnings, Dogecoin gained a massive following.

Community Engagement: The Dogecoin community, known for its enthusiastic and often lighthearted approach, became a significant force on social media platforms. They utilized platforms like Reddit, Twitter (and its successor, [X]), and Telegram to discuss the potential of Dogecoin, share memes, and rally support.

Influence of Social Media and Public Figures: The rise of Dogecoin to prominence was significantly bolstered by social media and high-profile endorsements. One notable example is Elon Musk, who frequently tweeted about Dogecoin, referring to it as the “people’s crypto.” His tweets often led to immediate spikes in Dogecoin’s value, illustrating the power of influential figures in the crypto community.

Community Initiatives: The Dogecoin community was also known for its charitable endeavors and quirky marketing stunts. For instance, they sponsored a NASCAR vehicle and funded the Jamaican Bobsled team’s trip to the Winter Olympics. These initiatives showcased the community’s collaborative spirit and ability to mobilize funds for causes and projects.

Impact and Lessons: Dogecoin’s journey highlighted several aspects unique to the cryptocurrency culture:

- Emotional Investment: Unlike traditional stocks or currencies, many Dogecoin investors were emotionally invested in the coin’s success, treating it as a part of their identity.

- Community Power: The ability of a united online community to influence the value and perception of a cryptocurrency.

- Risks and Volatility: The reliance on social media and influential figures for valuation can lead to significant volatility and risk for investors.

FOMO is Real

Many sat on the sidelines as Bitcoin rose from a few pennies to it’s current price of $39K. There are several stories of those who risked their entire life saving and are now multi-millionaires, and others, who sold hundreds of Bitcoins before its historic rise for a few pizzas. Either way, these stories fuel FOMO. Meme coins such as Dogecoin and Shiba Inu are relatively affordable in comparison and have a huge following. Many feel that it’s only a matter of time that Doge and Shiba will experience a similar rise.

The $1 Doge Dream

The ultimate goal of the doge fans is for dogecoin to reach $1. This will provide many HOLDers with a substantial gain in their investment and enable financial freedom for many. As of today’s writing, Dogecoin currently hovers around .086. For every $1000 invested a $1 target would equate to $11,628.

The 1 cent Shiba Dream

Shiba Inu fans dreams of a world / universe where it is worth 1 cent. At the current price of $0.000008, a $1000 investment would be worth $1.25 million.

There are many reasons why this will probably not occur in the near future, but that doesn’t mean anything to the faithful. They will continue to HODL for as long as it take to realize their dream. There’s not much to risk after the investment and almost everything to gain.

Crypto is the anti-establishment

Cryptocurrency represents the anti-establishment. Regarded as “the people’s coin,” these digital currencies offer a unique blend of technology, user empowerment, and a departure from conventional banking systems.

Decentralization as Empowerment

At the heart of the appeal of cryptocurrencies like Doge and Shiba Inu is their decentralized nature. Unlike traditional currencies, which are regulated by central banks and financial institutions, cryptocurrencies operate on decentralized networks, typically blockchain technology. This decentralization not only reduces the control of single entities over the currency but also offers greater transparency and security, appealing to those disillusioned with the traditional banking system.

Community-Driven Development

The developers of coins like Doge and Shiba Inu often maintain a close relationship with their user base, primarily through social media platforms. This direct interaction allows for a more democratic development process. Features, updates, and changes are frequently influenced by community feedback, making users feel more involved and invested in the currency’s trajectory. This sense of ownership and participation is rarely, if ever, found in traditional financial systems.

Beyond Financial Transactions

These cryptocurrencies have evolved to be more than mere mediums of exchange or investment vehicles. They have developed into cultural phenomena, with vibrant communities that not only talk about financial gains but also engage in charitable activities, social causes, and community events. This adds a layer of social responsibility and communal engagement to the currency, further strengthening its position as the people’s coin.

Crypto is the dream

Crypto inspires hope by creating a collective of like minded folks all itching for financial independence. It spans all walks of life, crosses diversity boundaries, and is mostly ignorant of political parties. There are some true crypto army’s out there that stand firm and HODL their coins regardless of its price. Their faith unshaken and believe carved in stone that they will be greatly rewarded for their patience. So they wait, for that fateful day. The day their chosen coin skyrockets 10000x, so they can live their life without financial worries or debt.

This unwavering belief in cryptocurrency transcends mere financial speculation. It represents a fundamental shift in how we perceive value, wealth, and the very notion of economic freedom. Crypto is not just about the potential financial windfall; it’s a symbol of a grassroots movement challenging traditional financial structures and offering an alternative vision of the future. It’s a testament to the power of collective belief and the enduring human spirit to seek autonomy in a rapidly changing world. As we stand on the brink of this financial frontier, it’s clear that crypto is more than just a digital asset — it’s a beacon of hope for many, a unifying force that defies traditional boundaries and empowers its adherents with the promise of a new financial dawn. Whether this dawn materializes as envisioned remains to be seen, but the journey towards it continues to captivate and inspire, signaling a significant shift in the global financial landscape.